Potato Processor Lamb Weston Reports Fiscal Third Quarter 2020 Results

Lamb Weston withdraws Fiscal Year 2020 Outlook due to uncertainty from the COVID-19 Pandemic’s Effect on Global Restaurant Traffic and Consumer Demand.

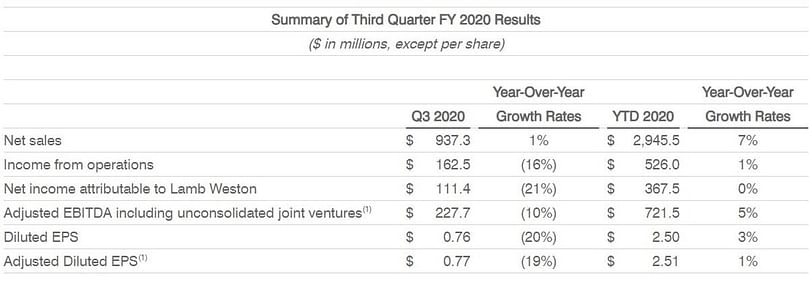

Lamb Weston Holdings, Inc. (NYSE: LW) announced its fiscal third-quarter 2020 results.

Tom Werner, President, and CEO at Lamb Weston Holdings, Inc :

“Our results in the third quarter were mixed.”Net sales for the Global segment, which is comprised of the top 100 North American based restaurant chain customers as well as the Company’s international business, decreased $11.1 million to $487.1 million, down 2 percent compared to the prior-year period. Volume decreased 1 percent, primarily due to higher sales of customized products and higher-margin limited-time offering products in the prior-year period, as well as the initial effects of the COVID-19 pandemic on restaurant traffic in China.

“We drove solid growth in our Foodservice and Retail segments, but our Global segment’s sales declined due to the timing of sales of customized products and higher-margin limited-time offering products, as well as the initial effects of the COVID-19 pandemic on restaurant traffic in China. In addition, all our segments had fewer shipping days related to the timing of the Thanksgiving holiday. We also realized the impact of higher-than-expected input and fixed cost inflation, which pressured earnings.”

“While the operating environment in most of our markets during the fiscal third quarter was favorable, estimates on the COVID-19 pandemic’s effect on the global economy are uncertain.”

“At this time, despite only two months remaining in our fiscal fourth quarter, we are unable to reasonably forecast frozen potato product demand because of the pandemic’s unpredictable near-term effect on restaurant traffic in North America and our key international markets. As a result, we’re withdrawing our financial outlook for the remainder of our fiscal year.”

“During these uncertain times, our top priorities are to ensure the health and welfare of our employees, maintain product safety, and continue to support our customers as they work to manage their supply chains and inventories. While the near-term impact of the COVID-19 pandemic on consumer demand and sales volume is likely to be material, we believe we have sufficient liquidity to manage through the uncertainty, and we remain confident in the long-term outlook for our customers and the continued growth of the global category.”

The Global segment sells the majority of the Company’s customized products, for which revenue is recognized when a purchase order is received to the extent the product has been manufactured, as opposed to sales of non-customized products, for which revenue is generally recognized upon shipment.

As a result, the timing of the receipt of a purchase order may create quarterly fluctuations in this segment. In addition, acquisitions contributed approximately 2 percentage points of volume growth, which was partially offset by an approximate 1 percentage point decline from the effect of fewer shipping days related to the timing of the Thanksgiving holiday.

Price/mix decreased 1 percent, largely due to unfavorable mix resulting from lower sales of customized products and limited-time offering products versus the prior-year period, customer mix in North America, and a higher proportion of growth in international sales volumes.

Global segment product contribution margin decreased $19.5 million to $109.3 million, down 15 percent compared to the prior-year period. Higher manufacturing costs due to input and fixed cost inflation, lower sales volumes, and unfavorable product and customer mix drove most of the decline.

The effect of the COVID-19 pandemic on consumer demand and manufacturing costs in China, higher transportation costs, and higher depreciation expense primarily associated with the new Hermiston production line, also pressured the segment’s profitability.

Foodservice

Net sales for the Retail segment, which includes sales of branded and private label products to grocery, mass merchant and club customers in North America, increased $3.2 million to $132.2 million, up 2 percent compared to the prior-year period. Price/mix increased 2 percent, largely driven by favorable mix.

Volume was flat as higher sales of Grown in Idaho and other branded products were offset by lower sales of private label products, as well as an approximate 2 percentage point impact from the effect of fewer shipping days related to the timing of the Thanksgiving holiday.

Retail segment product contribution margin decreased $0.3 million to $28.8 million, down 1 percent compared to the prior-year period, as input and fixed cost inflation, as well as higher transportation costs and depreciation expense primarily associated with the new Hermiston production line, more than offset favorable price/mix and lower advertising and promotional expenses.

Equity Method Investment Earnings

Equity method investment earnings from unconsolidated joint ventures in Europe, the U.S., and South America were $9.8 million and $14.2 million for the third quarter of fiscal 2020 and 2019, respectively. Earnings in the current quarter included a $2.6 million loss related to the withdrawal from a multiemployer pension plan by Lamb Weston RDO.

Equity method investment earnings also included a $7.3 million unrealized loss related to mark-to-market adjustments associated with currency and commodity hedging contracts in the current quarter and a $0.9 million loss related to these items in the prior-year quarter.

Excluding the Lamb Weston RDO pension-related comparability item and the mark-to-market adjustments, earnings from equity method investments increased $4.6 million compared to the prior-year period, largely reflecting lower raw potato prices and higher sales volumes in Europe.

Outlook

The Company has withdrawn its financial outlook for the fiscal year 2020 for net sales growth and for Adjusted EBITDA including unconsolidated joint ventures(1). At this time, the Company does not believe it can reasonably forecast frozen potato product demand in the near term due to the unpredictable near-term effect of the COVID-19 pandemic on the global economy, and more specifically, on restaurant traffic in North America and key international markets, including markets served by the Company’s joint ventures.

The Company’s previous outlook included the contribution of a 53rd week in the fiscal 2020 period, with the additional week falling in the fourth quarter.

The Company continues to expect for fiscal 2020:

- Interest expense of approximately $110 million;

- An effective tax rate(2) excluding comparability items of approximately 24 percent; and

- Depreciation and amortization of approximately $175 million.

In addition, the Company reduced its target for capital expenditures to approximately $200 million from approximately $300 million as the Company plans to defer certain capital expenditures.

End Notes

(1) Adjusted EBITDA including unconsolidated joint ventures and Adjusted Diluted EPS are non-GAAP financial measures. Please see the discussion of non-GAAP financial measures and the reconciliations at the end of this press release for more information.

(2) The effective tax rate is calculated as the ratio of income tax expense to pre-tax income, inclusive of equity method investment earnings.

(3) For more information about product contribution margin, please see the table titled 'Segment Information' in this press release.

Sponsored Content

Sponsored Content

Where

Sponsored Content

Search

Search

{kind=link}

{kind=link}