May registered a sharp increase in the value of the FAO Food Price Index

May registered a sharp increase in the value of the FAO Food Price Index

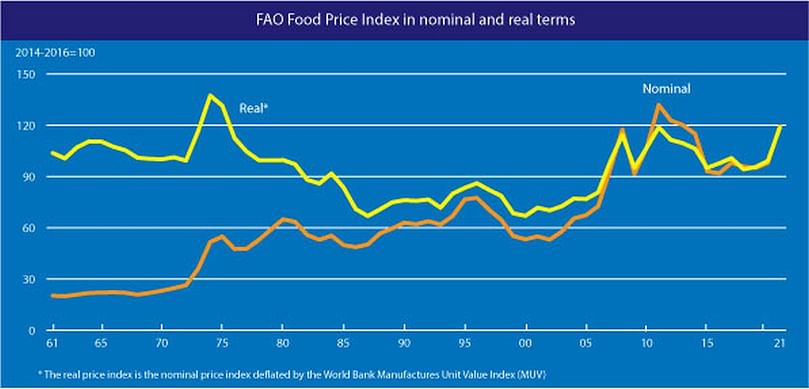

The FAO Food Price Index (FFPI) averaged 127.1 points in May 2021, 5.8 points (4.8 percent) higher than in April and as much as 36.1 points (39.7 percent) above the same period last year.

The May increase represented the biggest month-on-month gain since October 2010.

It also marked the twelfth consecutive monthly rise in the value of the FFPI to its highest value since September 2011, bringing the Index only 7.6 percent below its peak value of 137.6 points registered in February 2011.

The sharp increase in May reflected a surge in prices for oils, sugar, and cereals along with firmer meat and dairy prices.

The FAO Cereal Price Index averaged 133.1 points in May, up 7.6 points (6.0 percent) from April and 35.7 points (36.6 percent) above its May 2020 value.

Among the major cereals, international maize prices rose the most, gaining 12.9 points (8.8 percent) in May, reaching 75.6 points (89.3 percent) above their value last year and their highest level since January 2013.

Downgraded production prospects for Brazil added pressure to already tight global supplies amidst sustained strong demand.

However, towards the end of the month maize prices started to retreat, mostly in expectation of higher production prospects in the United States.

International barley and sorghum prices also increased in May, rising by 5.4 percent and 3.6 percent, respectively.

Following a surge in wheat prices in early May, improved crop conditions, particularly in the European Union and the United States, led to sharp price declines by the end of the month.

However, wheat prices still averaged 8.0 points (6.8 percent) up from April and 27.7 points (28.5 percent) above May 2020.

International rice prices held steady in May, with logistics and shipping costs keeping trading activity subdued through the month.

The FAO Vegetable Oil Price Index averaged 174.7 points in May, gaining 12.7 points (or 7.8 percent) month-on-month and marking a twelfth consecutive monthly rise.

The continued strength of the index mainly reflects rising palm, soy, and rapeseed oil values.

International palm oil quotations remained on an upward trajectory in May and reached their highest level since February 2011, as slow production growth in Southeast Asian countries, together with rising global import demand, kept inventories in leading exporting nations at relatively low levels.

As for soyoil, prospects of robust global demand, especially from the biodiesel sector, lent support to prices, while international rapeseed oil values were underpinned by continued global supply tightness.

The FAO Dairy Price Index averaged 120.8 points in May, up 1.7 points (1.5 percent) from April, marking one year of uninterrupted increases and lifting the value 26.4 points (28 percent) above its level of one year ago.

However, the index is still 22.8 percent below its peak value reached in December 2013.

In May, international quotations for skim milk powder rose the most, reflecting solid import demand amid limited spot supplies from the European Union, and those for whole milk powder increased on high import purchases, especially by China, despite New Zealand’s offer of large sales.

Cheese quotations also strengthened, mostly due to lower supplies from the European Union amidst strong demand. By contrast, butter prices fell on increased export supplies from New Zealand, marking the end of an eleven-month-long price rally.

The FAO Meat Price Index* averaged 105.0 points in May, up 2.3 points (2.2 percent) from April, registering the eighth monthly increase and lifting the index 10 percent above its level of one year ago, but still, nearly 12 percent below its peak reached in August 2014.

In May, price quotations for all meat types represented in the index rose, principally underpinned by a faster pace of import purchases by East Asian countries, mainly China.

Tightening global supplies also provided price support across all meat products, reflecting multiple factors ranging from slaughter slowdowns in the cases of bovine and ovine meats to rising internal demand for poultry and pig meats in leading producer regions.

The FAO Sugar Price Index averaged 106.7 points in May, up 6.8 points (6.8 percent) from April, marking the second consecutive monthly increase and the highest level since March 2017.

The rise in international sugar price quotations was mostly related to harvest delays and concerns over reduced crop yields in Brazil, the world's largest sugar exporter, as the prolonged dry weather conditions impacted crop development.

Additional support was provided by higher crude oil prices and a further strengthening of the Brazilian Real against the US dollar, which tends to restrain shipments from Brazil.

Large export volumes from India, however, contributed to easing the price surge and prevented larger monthly price gains.

*Unlike for other commodity groups, most prices utilized in the calculation of the FAO Meat Price Index are not available when the FAO Food Price Index is computed and published; therefore, the value of the Meat Price Index for the most recent months is derived from a mixture of projected and observed prices. This can, at times, require significant revisions in the final value of the FAO Meat Price Index which could in turn influence the value of the FAO Food Price Index.

(Click to enlarge)

Like to receive news like this by email? Join and Subscribe!

Get the latest potato industry news straight to your WhatsApp. Join the PotatoPro WhatsApp Community!

Highlighted Company

")

Related News

April 21, 2026

Spain: stronger agri-food border controls with more physical inspections

The government says that the reorganization of border controls made it possible to increase physical inspections of agri-food products by 7.5% in one year, strengthening oversight of imports and exports amid growing trade flows.

April 08, 2026

Europe: ecological requirements for the agro-industrial sector

All packaging placed on the EU market must be recyclable by 2030, while the industry is calling for more flexible requirements and extended timelines to clear existing stock.

April 04, 2026

FAO Food Price Index rises for a second consecutive month, driven mostly by energy‑related pressures on vegetable oil and sugar prices

The FAO Food Price Index* (FFPI) averaged 128.5 points in March 2026, up 3.0 points (2.4 percent) from its revised February level, marking a second consecutive month of increase.