FAO Food Price Index continued its upward trend in October

FAO Food Price Index continued its upward trend in October

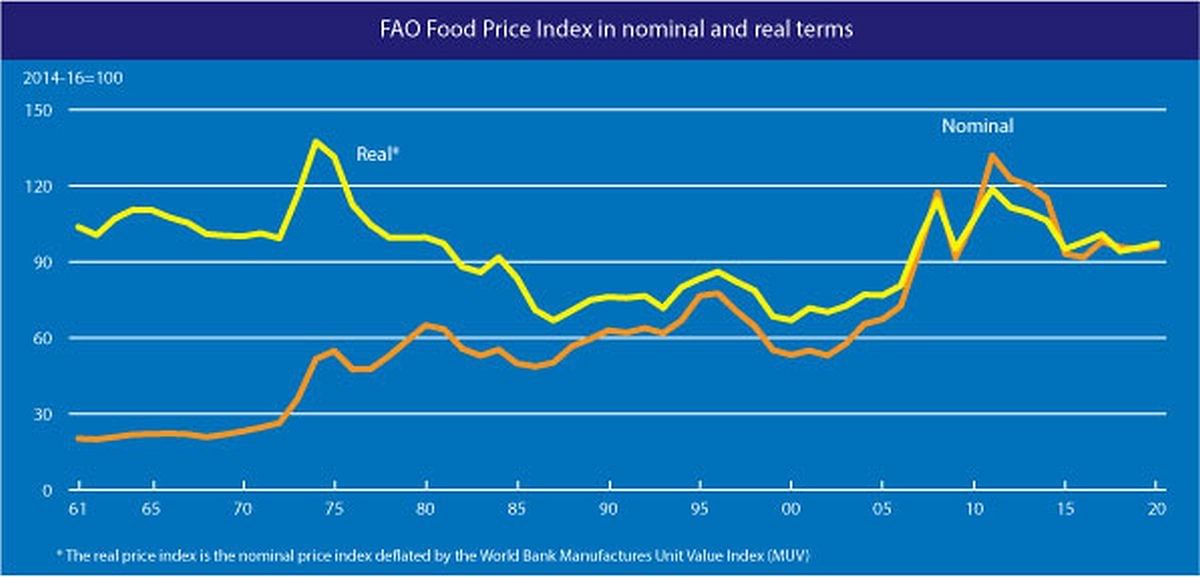

The FAO Food Price Index* (FFPI) averaged 100.9 points in October 2020, up 3.0 points (3.1 percent) from September and 5.7 points (6.0 percent) higher than its value a year ago.

The October value, the highest since January 2020, represented the fifth consecutive monthly increase. Much firmer prices of sugar, dairy, cereals, and vegetable oils were behind the latest rise in the FFPI, while the meat sub-index fell slightly for the second consecutive month.

The FAO Cereal Price Index averaged 111.6 points in October, up 7.5 points (7.2 percent) from September and as much as 15.8 points (16.5 percent) above its value in the corresponding month last year.

The October rise marked the fourth month of consecutive increase. Wheat export prices rose further in October, reflecting strong global demand amidst shrinking export availabilities, poor growing conditions in Argentina, and continued dry weather adversely affecting winter wheat conditions in parts of Europe, northern America, and the Black sea region.

International maize prices also rallied to over six-year highs, largely underpinned by a fast pace in purchases by China and higher than earlier anticipated drawdown of stocks in the United States of America as well as sharp declines in export supplies in Brazil and Ukraine.

Feed barley and sorghum prices also increased in October, supported by strong demand and spill-over from rising maize and wheat prices. By contrast, international rice prices fell to seven-month lows, as main-crop harvests got underway in Asia, intensifying efforts to attract buyers.

The FAO Vegetable Oil Price Index averaged 106.4 points in October, up 1.8 points (1.8 percent) month-on-month, and posting a nine-month high. The continued strength of the index largely reflects firmer palm and soy oil prices, while those of rapeseed oil declined moderately.

International palm oil quotations rose for a fifth consecutive month, underpinned by below-potential production prospects in leading producing countries and robust global import demand. In the meantime, soy oil values were supported by continued supply tightness in South America.

By contrast, after rising five months in succession, international rapeseed oil values decreased in October, amid increased uncertainty regarding demand in the EU following the recent deterioration of the COVID-19 situation across the region.

The FAO Dairy Price Index averaged 104.4 points in October, up 2.2 points (2.2 percent) from September, marking the fifth consecutive monthly increase and lifting the index 3.6 points (3.5 percent) above its value in the corresponding month last year.

In October, price quotations for all dairy products represented in the index rose, with cheese rising the most, followed by skim milk powder, whole milk powder, and butter.

Price increases in October reflected some degree of market tightening for near-term deliveries, underpinned by robust import demand from Asian and Middle Eastern markets amidst expectations for less export availabilities from Oceania later this year when production will be declining seasonally.

In addition, increases in internal demand for future deliveries in Europe, where production is nearing its seasonal low, also contributed to spot market tightening and price strengthening.

The FAO Meat Price Index** averaged 90.7 points in October, down slightly (0.5 points or 0.5 percent) from September, marking the ninth monthly decline since January, and standing 10.9 points (10.7 percent) lower than its value a year ago.

Pig meat prices dropped, as a fall in the quotations of German products, reflecting continued influence of the import restrictions imposed by China on Germany, outweighed an increase in those from Brazil due to robust import demand.

Meanwhile, bovine meat prices declined due to weak demand in the United States of America, coupled with rising shipments from South America, although supplies from Australia drifted lower due to rising demand for cattle for herd rebuilding. Poultry meat prices also fell slightly because of reduced orders from China and Saudi Arabia.

By contrast, prices of ovine meat rose on steady internal demand and low export supplies, especially in Australia.

The FAO Sugar Price Index averaged 85.0 points in October, up 6.0 points (7.6 percent) from September and 7.2 points (9.3 percent) from last year. This increase reflected mostly the prospects of a lower sugar output in both Brazil and India, the two largest sugar-producing countries, due to below-average rainfalls.

Sugar prices were also supported by developments in Thailand, where sugar output is seen lower by almost 5 percent from last year as a result of protracted dry conditions.

Additional upward pressure was provided by fund buying, as evidenced by the weekly Commitment of Traders (COT) report. Furthermore, sugar prices displayed high volatility, driven also by uncertainties in crude oil market and movements in the Brazilian Real against the United States Dollar.

* Effective July 2020, the price coverage of the FFPI has been expanded and its base period revised to 2014-2016. For more details on this revision, please see the feature article of the June 2020 issue of the Food Outlook.

** Unlike for other commodity groups, most prices utilized in the calculation of the FAO Meat Price Index are not available when the FAO Food Price Index is computed and published; therefore, the value of the Meat Price Index for the most recent months is derived from a mixture of projected and observed prices. This can, at times, require significant revisions in the final value of the FAO Meat Price Index which could in turn influence the value of the FAO Food Price Index.

(Click to enlarge)

Like to receive news like this by email? Join and Subscribe!

Get the latest potato industry news straight to your WhatsApp. Join the PotatoPro WhatsApp Community!

Highlighted Company

")

Related News

April 21, 2026

Spain: stronger agri-food border controls with more physical inspections

The government says that the reorganization of border controls made it possible to increase physical inspections of agri-food products by 7.5% in one year, strengthening oversight of imports and exports amid growing trade flows.

April 08, 2026

Europe: ecological requirements for the agro-industrial sector

All packaging placed on the EU market must be recyclable by 2030, while the industry is calling for more flexible requirements and extended timelines to clear existing stock.

April 04, 2026

FAO Food Price Index rises for a second consecutive month, driven mostly by energy‑related pressures on vegetable oil and sugar prices

The FAO Food Price Index* (FFPI) averaged 128.5 points in March 2026, up 3.0 points (2.4 percent) from its revised February level, marking a second consecutive month of increase.