Lamb Weston Holdings, Inc. (NYSE: LW) announced today its fiscal second quarter 2020 results. Updates Fiscal Year 2020 Outlook.

Lamb Weston Reports Fiscal Second Quarter 2020 Results

Last week Lamb Weston Holdings, Inc. (NYSE: LW) announced its fiscal second quarter 2020 results.

Second Quarter 2020 Highlights

- Net sales increased 12% to $1,019 million

- Income from operations increased 11% to $194 million

- Net income increased 18% to $140 million

- EBITDA including unconsolidated joint ventures(1) increased 17% to $261 million

- Diluted EPS increased 28% to $0.95 from $0.74

- Adjusted Diluted EPS(1) increased 19% to $0.95 from $0.80

Updated FY 2020 Outlook

- Net sales expected to increase at the high end of the Company’s estimate of mid-single digit growth

- Adjusted EBITDA including unconsolidated joint ventures(1) expected to be $965 million-$985 million, up from the previous estimate of $950 million-$970 million.

Capital Deployment Highlights

- Increased quarterly dividend by 15% to $0.23 per share, payable on February 28, 2020

- Returned $72 million of cash to shareholders in the first half of fiscal 2020

- Invested $17 million of cash in the quarter for a 50% interest in an Argentinian frozen potato processing joint venture

Tom Werner, President and CEO:

“In the second quarter, we delivered strong sales, volume and earnings growth across each of our core business segments by continuing to execute well across the organization.”

“We’re generating strong cash flow, and we’re investing that cash back into the business to support customer growth, improve manufacturing operations and systems, and bolster our presence in key markets such as Australia and South America. We’re also returning more cash to shareholders, including recently raising our quarterly dividend by 15 percent.”

“Because of our strong performance in the first half of fiscal 2020, we have raised our annual outlook for sales growth and EBITDA. We anticipate delivering solid results in the second half of the year, supported by continued favorable restaurant traffic trends.”

“While overall raw potato supply in North America and Europe is tight due to relatively poor weather late in the growing season and during the harvest, we expect to have enough raw potatoes to support our volume growth targets for the year.”

“We’ll continue to evaluate opportunities to improve price and mix in each of our business segments. Over the long term, we remain committed to executing on our strategies, driving growth and creating value for all our stakeholders.”

(Click to enlarge)

Summary of Second Quarter FY 2020 Results

Q2 2020 Commentary

Net sales increased $107.8 million to $1,019.2 million, up 12 percent versus the year-ago period. Volume increased 10 percent, primarily driven by growth in the Company’s Global and Foodservice segments, and includes an approximate 1.5 percentage point benefit from acquisitions, as well as an approximate 1 percentage point benefit from additional shipping days related to the timing of the Thanksgiving holiday. Price/mix increased 2 percent due to pricing actions and favorable mix.

Income from operations rose 11 percent to $193.5 million versus the year-ago period, driven by higher sales and gross profit. Gross profit increased $36.1 million due to volume growth, favorable price/mix and lower transportation costs, which more than offset input cost inflation; higher manufacturing costs due to inefficiencies, which were primarily driven by higher maintenance and related costs; and higher depreciation expense primarily associated with the Company’s french fry production line in Hermiston, Oregon, which started operating towards the end of the fourth quarter of fiscal 2019.

In addition, gross profit included a $3.9 million gain related to unrealized mark-to-market adjustments and realized settlements associated with commodity hedging contracts in the current quarter, compared with a $1.7 million loss related to these items in the prior year quarter.

The increase in gross profit in the current quarter was partially offset by a $16.6 million increase in selling, general and administrative expenses (“SG&A”). The increase was largely driven by an approximate $6 million increase in incentive compensation expense accruals based primarily on the Company’s operating performance, as well as investments in the Company’s sales, marketing, operating and systems capabilities, which included more than $2 million of expense associated with designing and implementing a new enterprise resource planning (“ERP”) system.

These increases were partially offset by an approximate $2 million reduction in foreign exchange losses. The prior year period also included an approximate $4 million insurance settlement benefit.

Net income attributable to Lamb Weston increased $21.4 million, or 18 percent, to $140.4 million, primarily reflecting growth in income from operations and higher equity method earnings, as well as an approximate $5 million benefit from acquiring the remaining 50.01% equity interest in the Company’s joint venture, Lamb Weston BSW, LLC (“Lamb Weston BSW”) in November 2018 (the “BSW Acquisition”).

EBITDA including unconsolidated joint ventures(1) increased $38.1 million to $260.9 million, up 17 percent versus the prior year period, primarily due to growth in income from operations, an approximate $6 million incremental benefit from the BSW Acquisition, and higher equity method investment earnings.

Diluted EPS increased $0.21, or 28 percent, to $0.95. The increase largely reflects growth in income from operations and higher equity method investment earnings, as well as an approximate $0.04 benefit from the BSW Acquisition, and a $0.06 charge related to the BSW Acquisition in the prior year period.

Adjusted Diluted EPS(1) increased $0.15, or 19 percent, to $0.95. The increase in Adjusted Diluted EPS reflects growth in income from operations, an approximate $0.04 benefit from the BSW Acquisition, and higher equity method investment earnings.

The Company’s effective tax rate(2) in the second quarter of fiscal 2020 was approximately 23.3 percent, versus 21.5 percent in the prior year period. The effective tax rate varies from the U.S. statutory tax rate of 21% principally due to the impact of U.S. state taxes, foreign taxes, permanent differences, and discrete items.

Cash Flow

Through the first half of fiscal 2020, net cash from operating activities increased $28.5 million to $345.3 million, primarily driven by earnings growth. Capital expenditures, including for information technology items, were $107.4 million in fiscal 2020, down $63.0 million versus the prior year period due to investments for the construction of a new production line in Hermiston, Oregon, which was completed in the fourth quarter of fiscal 2019.

Capital Returned to Shareholders

In the first half of fiscal 2020, the Company returned a total of $71.9 million to shareholders, including $58.5 million in dividends and $13.4 million in share repurchases. The average price per share repurchased was $72.61. The Company has approximately $205 million remaining under its current $250 million share repurchase authorization.

Full Financial Release

For the full financial release, including additional details, the outlook for the remainder of 2020, as well as the explanations of the notes, we refer to the Lamb Weston Holdings website

Q2 2020 Segment Highlights

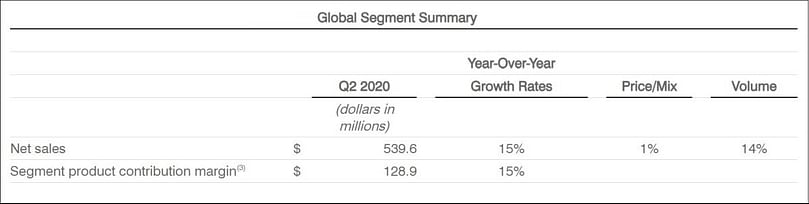

Global Segment Summary

(Click to enlarge)

Net sales for the Global segment, which is comprised of the top 100 North American based restaurant chain customers as well as the Company’s international business, increased $69.6 million to $539.6 million, up 15 percent compared to the prior year period. Volume increased 14 percent, driven by growth in sales, including the benefit of limited time product offerings, to strategic customers in the U.S. and key international markets, as well as an approximate 3 percentage point benefit from acquisitions.Approximately 1 percentage point of the volume increase reflected the benefit of additional shipping days related to the timing of the Thanksgiving holiday. Price/mix increased 1 percent, largely reflecting pricing adjustments associated with multi-year contracts.

Global segment product contribution margin increased $16.5 million to $128.9 million, up 15 percent compared to the prior year period. Favorable volume growth, higher price/mix and lower transportation costs drove the increase, more than offsetting input cost inflation, higher manufacturing costs due to inefficiencies, and higher depreciation expense primarily associated with the new Hermiston production line.

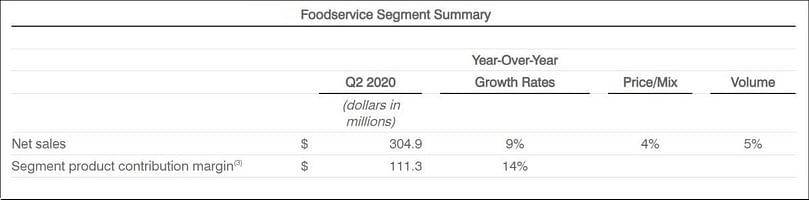

Foodservice Segment Summary

(Click to enlarge)

Net sales for the Foodservice segment, which services North American foodservice distributors and restaurant chains outside the top 100 North American based restaurant chain customers, increased $25.2 million to $304.9 million, up 9 percent compared to the prior year period. Volume increased 5 percent, led by growth in distributor private label and Lamb Weston branded products.Approximately half of the volume increase reflected the benefit of additional shipping days related to the timing of the Thanksgiving holiday. Price/mix increased 4 percent, primarily reflecting pricing actions initiated during the quarter, and improved mix.

Foodservice segment product contribution margin increased $13.9 million to $111.3 million, up 14 percent compared to the prior year period, as favorable price/mix, volume growth and lower transportation costs more than offset input cost inflation, higher manufacturing costs due to inefficiencies, and higher depreciation expense primarily associated with the new Hermiston production line.

Retail Segment Summary

(Click to enlarge)

Net sales for the Retail segment, which includes sales of branded and private label products to grocery, mass merchant and club customers in North America, increased $8.2 million to $132.1 million, up 7 percent compared to the prior year period. Volume increased 4 percent, driven by increased sales of Grown in Idaho and other branded products as well as private label products.Approximately 2 percentage points of the volume increase reflected the benefit of additional shipping days related to the timing of the Thanksgiving holiday. Price/mix increased 3 percent, driven by favorable mix and pricing actions.

Retail segment product contribution margin increased $2.6 million to $28.5 million, up 10 percent compared to the prior year period, as favorable price/mix, volume growth and lower transportation costs, more than offset input cost inflation, higher manufacturing costs due to inefficiencies, and higher depreciation expense, primarily associated with the new Hermiston production line.

Outlook

As summarized in the table above, for fiscal 2020, the Company expects:

- Net sales to grow at the high end of the mid-single digit range, largely driven by volume as well as modestly higher price/mix.

- Adjusted EBITDA including unconsolidated joint ventures(1) in the range of $965 million to $985 million, an increase from the Company’s previous estimate of $950 million to $970 million. The Company expects:

- Volume-driven gross profit growth, with higher price/mix offsetting input cost inflation;

- SG&A, excluding advertising and promotional expenses and investments to upgrade the Company’s enterprise resource planning and other information systems infrastructure, to be 8.0 percent to 8.5 percent of net sales.

- Equity method investment earnings to improve versus fiscal 2019, reflecting the effects of lower raw potato costs in Europe.

- An effective tax rate of approximately 24 percent versus the Company’s previous estimate of 23 to 24 percent.

Like to receive news like this by email? Join and Subscribe!

Get the latest potato industry news straight to your WhatsApp. Join the PotatoPro WhatsApp Community!

Highlighted Company

Related News

July 23, 2026

APEDA Facilitates Uttarakhand’s First Frozen French Fries Export to Iraq

APEDA facilitated Uttarakhand's first frozen French fries export, shipping a 24-tonne consignment from Kashipur to Iraq. The milestone expands value-added potato exports and supports better market access, logistics, and future export growth in India.

July 17, 2026

Lamb Weston to showcase new potato innovations at WOFEX 2026

Lamb Weston will showcase Snap Fries, Frenzy Fries and Original Mash Cup at WOFEX 2026 in Manila, highlighting potato innovations designed to help airlines and foodservice operators improve efficiency, flexibility and menu differentiation.

July 14, 2026

Best Frozen Sweet Potato Fries Ranked: Alexia, Ore-Ida, and Sprouts Lead the Taste Test

A taste test of six frozen sweet potato fry brands ranked Alexia as the best overall for flavor and texture, Ore-Ida as the crispiest, and Sprouts as the top honorable mention, highlighting top picks for burgers, sandwiches, and more.