The FAO Food Price Index continues to rise unabated.

The FAO Food Price Index continues to rise unabated

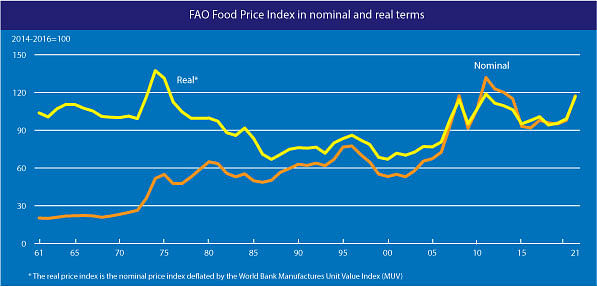

The FAO Food Price Index (FFPI) averaged 120.9 points in April 2021, 2.0 points (1.7 percent) higher than in March, and as much as 28.4 points (30.8 percent) above the same period last year.

The increase marked the eleventh consecutive monthly rise in the value of the FFPI to its highest level since May 2014. The April rise was led by strong increases in the prices of sugar, followed by oils, meat, dairy, and cereals.

The FAO Cereal Price Index averaged 125.1 points in April, up 1.5 points (1.2 percent) from March, resuming its climb after a short-lived one-month respite in March, and stood 25.8 points (26.0 percent) above its April 2020 level.

Upward pressure from smaller-than-anticipated planting intentions in the United States of America (USA) and concerns about crop conditions in Argentina, Brazil, and the USA pushed maize prices up 5.7 percent in April.

With overall tightening maize supplies, on top of continued strong demand, maize prices stood 66.7 percent above their values one-year-earlier and remain at their highest level since mid-2013.

Among other coarse grains, international barley, and sorghum prices continued to soften, falling 1.2 and 1.0 percent in April but remained 26.8 and 86.5 percent above their respective values in the corresponding month last year.

International wheat prices were generally steady in April, remaining over 17 percent above their April 2020 values.

While wheat quotations received support from rising maize prices, along with crop condition concerns in the USA and several countries in Europe, the expectations for good global production prospects kept prices generally stable.

By contrast, international rice prices decreased again in April, mainly reflecting currency movements and slow trading activities, with persistent logistical constraints and freight costs continuing to hinder fresh deals.

The FAO Vegetable Oil Price Index averaged 162.0 points in April, up 2.9 points (1.8 percent) month-on-month, driven by rising soy, rapeseed, and palm oil quotations more than offsetting lower sunflower oil values.

International palm oil prices continued to rise in April on concerns over slower-than-expected production growth in major exporting countries.

Soy and rapeseed oil values climbed further too, underpinned by, respectively, firm global demand, including from biodiesel producers, and protracted global supply tightness. By contrast, international prices of sunflower oil contracted moderately on-demand rationing.

The FAO Dairy Price Index averaged 118.9 points in April, up 1.4 points (1.2 percent) from March, rising for the eleventh consecutive month and lifting the index 24.1 percent above its value a year ago.

In April, butter quotations rose, underpinned by solid import demand from Asia, notwithstanding weaker internal demand in Europe. Skim milk powder prices increased due to high import demand from East Asia, induced partly by concerns over potential shipping delays amid limited spot supplies from Europe and Oceania.

Cheese prices also increased due to high demand from Asia, amid lower-than-expected production in Europe and seasonally declining supplies from Oceania.

By contrast, quotations for whole milk powder declined slightly, reflecting lower import demand for the available supplies, following significantly high volumes traded recently.

The FAO Meat Price Index* averaged 101.8 points in April, up 1.7 points (1.7 percent) from the slightly revised value for March, marking a seventh consecutive monthly increase and raising the index by 5.1 percent above the corresponding month last year.

In April, bovine and ovine meat quotations rose, underpinned by solid demand from East Asia, amidst tight supplies from Oceania due to ongoing herd rebuilding and low inventories.

Elevated internal sales in some producing regions also supported bovine and ovine meat prices. Pig meat quotations firmed on continued high purchases by East Asia, despite increased overall shipments from the European Union, while Germany continued with no access to the Chinese market over African swine fever concerns. Meanwhile, poultry meat prices remained steady, reflecting generally balanced global markets.

The FAO Sugar Price Index averaged 100.0 points in April, up 3.8 points (3.9 percent) from March and reaching levels nearly 60 percent above those registered in the corresponding month last year.

The April rebound in international sugar price quotations was prompted by strong buying amid heightened concerns over tighter global supplies in 2020/21, due to the slow harvest progress in Brazil and frost damage in France.

Further support was provided by the strengthening of the Brazilian Real against the US Dollar, which tends to affect shipments from Brazil, the world's largest sugar exporter.

However, the upward pressure on prices was somewhat limited by prospects of large exports from India and the slight decline in crude oil prices.

*Unlike for other commodity groups, most prices utilized in the calculation of the FAO Meat Price Index are not available when the FAO Food Price Index is computed and published; therefore, the value of the Meat Price Index for the most recent months is derived from a mixture of projected and observed prices. This can, at times, require significant revisions in the final value of the FAO Meat Price Index which could in turn influence the value of the FAO Food Price Index.

(Click to enlarge)

Like to receive news like this by email? Join and Subscribe!

Get the latest potato industry news straight to your WhatsApp. Join the PotatoPro WhatsApp Community!

Highlighted Company

")

Related News

April 21, 2026

Spain: stronger agri-food border controls with more physical inspections

The government says that the reorganization of border controls made it possible to increase physical inspections of agri-food products by 7.5% in one year, strengthening oversight of imports and exports amid growing trade flows.

April 08, 2026

Europe: ecological requirements for the agro-industrial sector

All packaging placed on the EU market must be recyclable by 2030, while the industry is calling for more flexible requirements and extended timelines to clear existing stock.

April 04, 2026

FAO Food Price Index rises for a second consecutive month, driven mostly by energy‑related pressures on vegetable oil and sugar prices

The FAO Food Price Index* (FFPI) averaged 128.5 points in March 2026, up 3.0 points (2.4 percent) from its revised February level, marking a second consecutive month of increase.

, and Potato Leafroll Virus (PLRV) to support more sustainable potato production with reduced reliance on crop protection chemicals.")