The FAO Food Price Index reached a 26-month high in November

The FAO Food Price Index reached a 26-month high in November

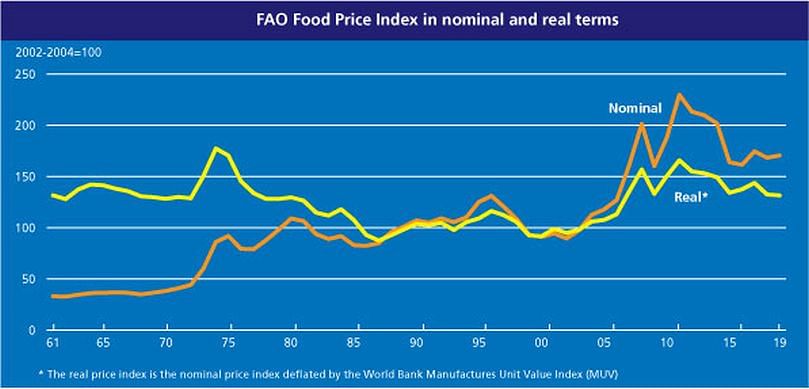

The FAO Food Price Index* (FFPI) averaged 177.2 points in November 2019; up 4.7 points (2.7 percent) from October and 15.4 points (9.5 percent) from the corresponding period last year.

The November hike from the previous month, mostly driven by significant surges in the prices of meat and vegetable oils, pushes the overall FFPI value to its highest level since September 2017.

Sugar prices also increased in November, while the dairy sub-index remained steady and cereal prices drifted lower.

The FAO Cereal Price Index averaged 162.4 points in November, down 1.9 points (1.2 percent) from October. Large export supplies and stiff competition among the world’s leading exporters weighed on international wheat prices, while rice values also fell in November, to six-month lows, pressured by new crop arrivals and sluggish import demand.

In the coarse grains market, US maize export prices remained under down pressure amid slow pace in sales, while export quotations from other origins, in particular Argentina and Brazil, were generally firmer on strong domestic as well as international demand.

The FAO Vegetable Oil Price Index averaged 150.6 points in November, up 14.2 points (10.4 percent) from October and marking the highest level since May 2018. The rise was led by firming palm oil values, while also soy, rapeseed and sunflower oil prices increased.

International palm oil quotations rose for the fourth consecutive month, extending the rebound in prices from the multi-year lows registered since late 2018. In addition to earlier-than-expected production slowdowns in major producing countries, the increase in palm oil prices was fuelled by robust global import demand, increased utilization for biodiesel and expectations of possible supply shortages next year.

While palm oil values were behind the increase in prices throughout the vegetable oil complex, rapeseed and soy oil values also received support from, respectively, continued supply tightness and sustained demand from the biofuel sector.

The FAO Dairy Price Index averaged almost 192.6 points in November, registering only a marginal increase from October, after two months of declines. At this level, the index is 16.8 points (9.5 percent) above the corresponding month last year. In November, international price quotations for skim milk powder (SMP) and whole milk powder (WMP) rose the most, reflecting tighter availability of spot supplies, as milk production in Europe entered its seasonal low, amid brisk global import demand.

After two months of declines, butter quotations rose slightly due to good overall demand, notwithstanding ample export availabilities. Cheese prices fell for a third consecutive month, as available supplies somewhat exceeded the demand.

The FAO Meat Price Index* averaged 190.5 points in November, up 8.4 points (4.6 percent) from October, representing the largest month-on-month increase since May 2009. At this level, the index is almost 28 points (17.2 percent) above its value a year ago, but still 21.5 points (9.4 percent) below the peak reached in August 2014.

Price quotations for all types of meat represented in the Index firmed, with those of bovine and ovine rising the most, reflecting tight export availabilities against persistent strong import demand, especially from China.

Demand led by end-of-the-year festivities exacerbated the tightening of global meat markets, lifting pig meat prices further and resulting in some increase in poultry meat prices after three months of declines.

The FAO Sugar Price Index averaged 181.6 points in November, up 3.3 points (1.8% percent) from October. The latest increase in international sugar prices came on the back of mounting indications that world sugar consumption would surpass production in the 2019/20 season.

Less than ideal growing conditions in Thailand, India, France and the United States raised chances for marked production setbacks and a reduction in global stocks. Large speculative movements amid uncertainties related to crop conditions, coupled with mixed prospects in the crude oil market, contributed to more volatile sugar futures prices in recent weeks.

* Unlike for other commodity groups, most prices utilized in the calculation of the FAO Meat Price Index are not available when the FAO Food Price Index is computed and published; therefore, the value of the Meat Price Index for the most recent months is derived from a mixture of projected and observed prices. This can, at times, require significant revisions in the final value of the FAO Meat Price Index which could in turn influence the value of the FAO Food Price Index.

Like to receive news like this by email? Join and Subscribe!

Get the latest potato industry news straight to your WhatsApp. Join the PotatoPro WhatsApp Community!

Highlighted Company

")

Related News

July 30, 2026

The Potato Project opens first flagship gourmet potato restaurant in Mumbai

The Potato Project will open its first flagship outlet in Mumbai on 31 July, introducing a gourmet potato-focused QSR concept. Built around white potato, purple potato and yam, the brand plans to expand across India and into international markets.

April 21, 2026

Spain: stronger agri-food border controls with more physical inspections

The government says that the reorganization of border controls made it possible to increase physical inspections of agri-food products by 7.5% in one year, strengthening oversight of imports and exports amid growing trade flows.

April 08, 2026

Europe: ecological requirements for the agro-industrial sector

All packaging placed on the EU market must be recyclable by 2030, while the industry is calling for more flexible requirements and extended timelines to clear existing stock.